Recommended Articles

How the Belt and Road Initiative is opening up business opportunities

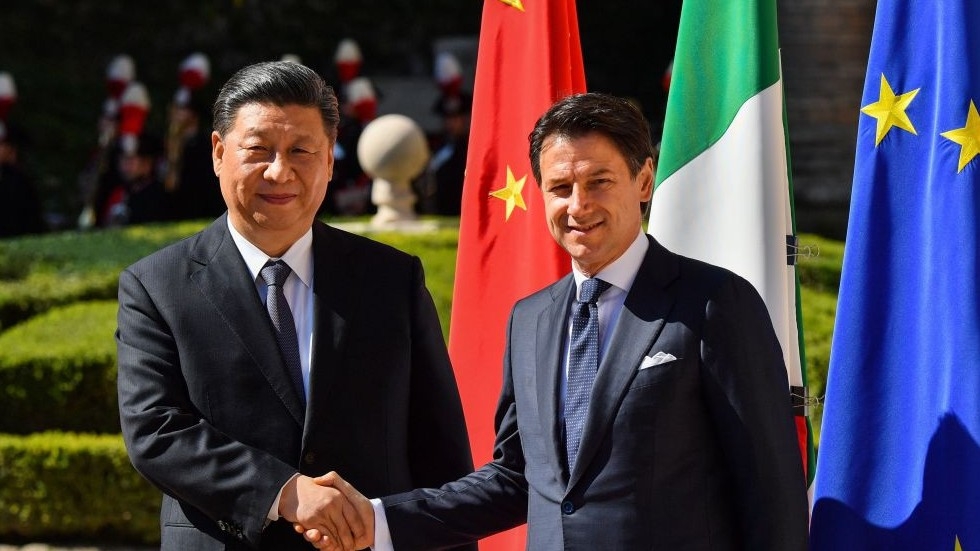

Italy and the Belt and Road Initiative: Rome’s Overture to Beijing

Myths Versus Facts – Is China’s Belt and Road Initiative really a “predatory debt trap”?